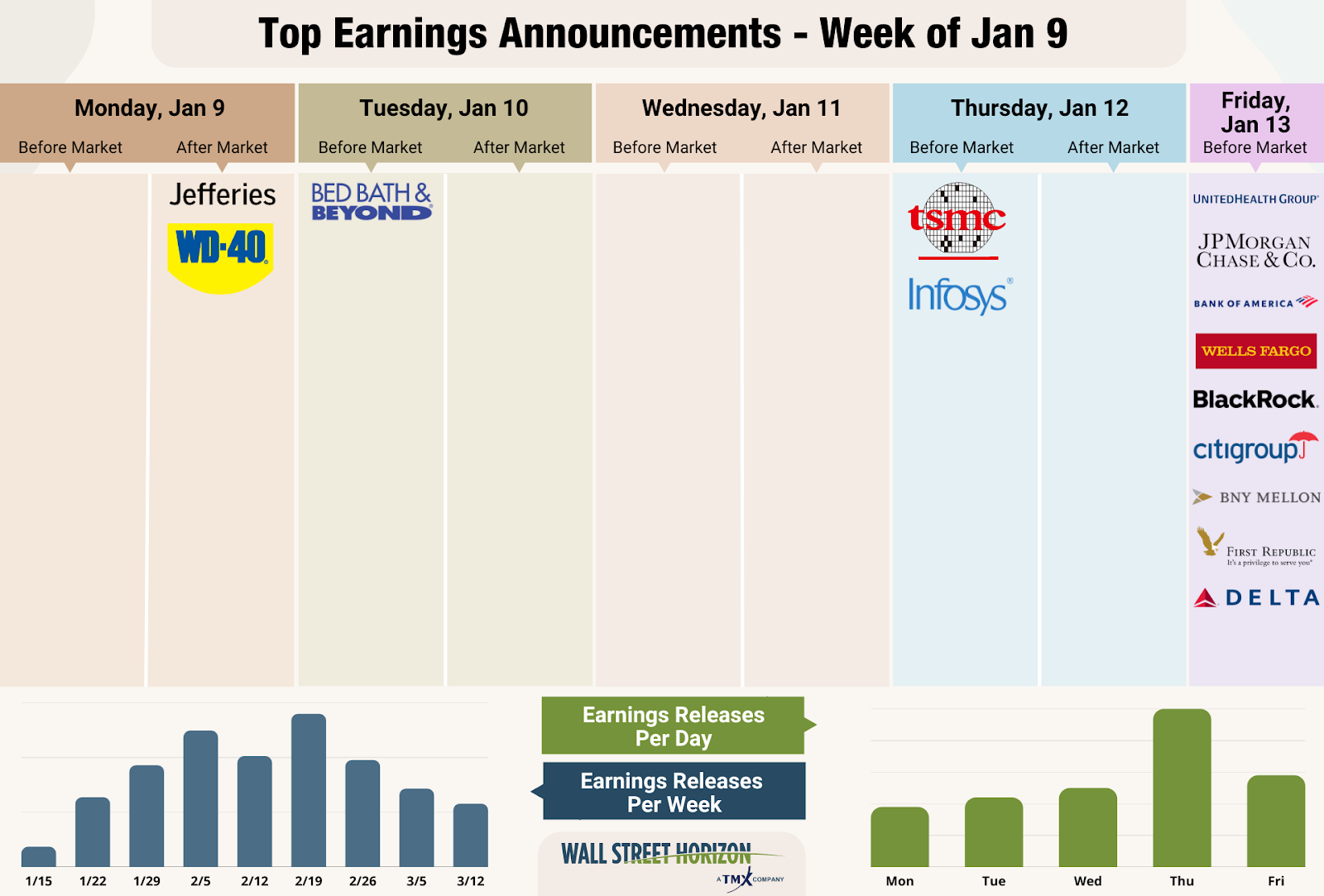

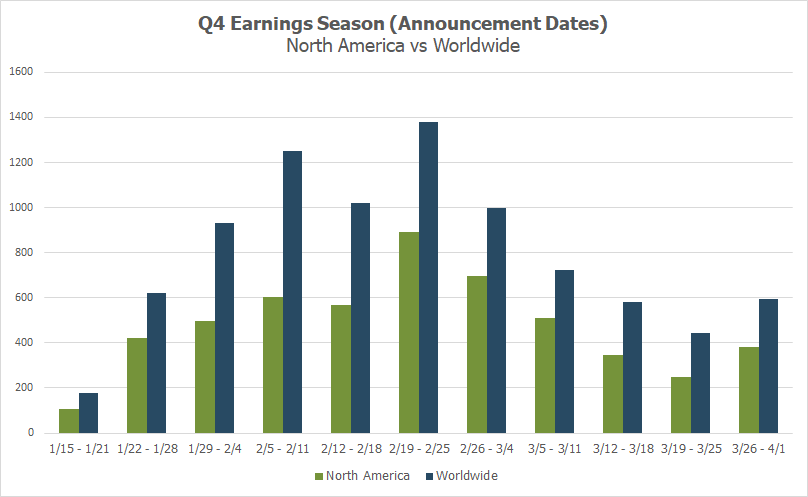

Key Takeaways: S&P 500 EPS growth for Q4 is set to come in at -4.1%, the lowest rate in over 2 years Themes from Q4 and for 2023: inflation, increasing interest rates, possibility of recession Despite headwinds, an early reading of corporate uncertainty seems to indicate that companies are feeling better about business conditions in 2023 Laggards from Q4 include Materials, Consumer Discretionary and Comm Services Big banks kick things off with JPM, BAC, C and WFC reporting Friday Peak weeks for Q4 season from January 30 - March The Q4 2022 earnings season kicks off with reports from the big banks this Friday the 13th, which seems like a particularly bad omen if you also consider that growth is anticipated to take a meaningful dip. This is expected to be the first quarterly decline in over 2 years, with S&P 500 EPS growth estimated to come in at -4.1% vs. the -5.7% recorded in Q3 2020 as the world was in the midst of a pandemic.¹ To learn more about what we look for during earnings season catch my recent interview on The Investing for Beginners podcast. Same As it Ever Was: Headwinds from Earlier in the Year Remain US companies continued to face a number of headwinds in the final quarter of the year, among them inflation remained the largest deterrent to growth for certain sectors. Despite the fact that measures of inflation including CPI and PPI began to ease towards the end of the year, many companies still had to contend with higher costs for labor, fuel and materials, lowering revenues and squeezing margins. Stubbornly high inflation caused the Fed to continue their march towards a Fed Funds Rate of 5 - 5.25%. An economy that continued to remain hot despite these rate changes, as well as a tight employment situation will likely mean the Fed stays on course with rate increases in 2023 as they have indicated, with no reductions until 2024. The possibility of a recession was also top of mind for companies last year, with approximately 36% of S&P 500 corporations mentioning it on earnings calls last quarter. However, that was down from 48% in Q2 2022, showing corporate anxiety was slowing. Corporate Uncertainty Appears to Be Easing Another measure of corporate uncertainty that seems to be signaling brighter skies ahead is the Late Earnings Report Index or LERI. The pre-peak LERI index (calculated the Friday that banks report) isn’t due out until Friday morning but it’s already showing surprisingly strong corporate body language about the upcoming earnings season, just as it did last quarter. In the face of the aforementioned headwinds, the LERI is pointing toward a positive earnings season. Notably, more companies are scheduling their earnings announcements significantly earlier than normal compared to the number of companies who are pushing their announcement dates back significantly. Currently the measure is on track to show the lowest reading since 2018. Laggards of Q4 - Materials, Consumer Discretionary & Communication Services So who were the main contributors to weakness in Q4? According to FactSet, 7 of the 11 S&P 500 sectors are expected to show a decline in YoY EPS growth for Q4, with only 3 expected to show a decline in revenues. Materials are expected to show the largest YoY drop in earnings growth, down 24% as higher interest rates and a decline in global growth weigh on the companies in that sector. This comes after a burst in growth in the first quarter, as the The S&P/TSX Composite Materials Index peaked in mid-April, when Russia’s invasion of Ukraine caused commodity prices to skyrocket. Following Materials is Consumer Discretionary, expected to see profits fall 19.5%. The holiday shopping season wasn’t as strong as expected, and November Retail Sales fell more than anticipated at -0.6%. Friday we’ll get the December reading. The retailers leading the sector lower include Amazon, expected to see YOY EPS decrease 86% and Target expected to be down 56%. While travel and leisure has been a strong point for the sector, certain names such as MGM Resorts, Wynn and Las Vegas Sands are all down. Communications Services is the third largest laggard at -18.5%, led by those that have been impacted by lower ad spend in 2022, mainly Alphabet (GOOGL) and Meta Platforms (META). Banks Kick it Off Friday The fourth largest laggard in Q4? You guessed it, the Financials. The expected growth rate currently stands at -12.2%, and that’s moved down from -4.3% on September 30. A decrease in M&A and IPO activity, as well as corporate and mortgage lending has eaten into profits and necessitated some of the large workforce reduction plans recently announced by the world’s biggest banks. On Friday we’ll hear from: JPMorgan Chase (JPM) - Earnings release BMO, conference call 8:30AM EDT Our DateBreaks factor uncovered two unusual (and positive) dates for banks. The Bank of New York Mellon was expected to post results on January 18 due to their historical reporting date, yet they confirmed for January 13, a full 5 days earlier. Wells Fargo originally confirmed a report date for Wednesday January 18, only to change it to Friday, January 13 on November 9. Source: Wall Street Horizon Earnings Wave This season peak weeks will fall between January 30 - March 3, with each week expected to see over 1,000 reports. Currently February 23 is predicted to be the most active day with 773 companies anticipated to report. Thus far only 21% of companies have confirmed their earnings date (out of our universe of 9,500+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data. Keep in mind the Q4 reporting season is always a bit more prolonged, typically stretching over 4 or 5 peak weeks rather than the usual 3 peak weeks seen in Q1 - Q3. Source: Wall Street Horizon

BlackRock (BLK) - Earnings release BMO, conference call 8:30AM EDT

Bank of America (BAC) - Earnings release BMO, conference call 9:30AM EDT

The Bank of New York Mellon (BK) - Earnings release BMO, conference call 10:00AM EDT

Citigroup Inc. (C) - Earnings release BMO, conference call 11:00AM EDT

Wells Fargo & Co. (WFC) - Earnings release BMO, conference call 12:00PM EDT

Recent Content

-

_thumb.png)

Volatility Watch: Eyeing a Pair of Blue Chips with Unusual Earnings Dates in the Heart of the Reporting Season

-

_thumb.png)

The Magnificent 7 Get Set to Report Amidst an S&P 500 Losing Streak

-

_thumb.png)

CEO Uncertainty Spikes After Improving Last Quarter

-

_thumb.png)

Earnings Season Heats Up, Spotting Two Unusual Reporting Dates in the Consumer Space

-

CNBC: Brace Yourself for Short-Term Volatility

-

Cheddar: It's Not Just You: The ‘Vibes Are a Little Off’ in This Economy

-

Data Minds - Triple Threat: Leveraging Data to Manage AI, ESG, and ETF Risks | April 11, 2024 [Recording Available]

-

Seeking Alpha: Q1 2024 Earnings Preview: Will Reports Be Good Enough To Turn Markets Positive

-

BNN Bloomberg: Markets today: 'Mag Seven' power stocks in run-up to U.S. earnings

-

_thumb.png)

Q1 2024 Earnings Preview: Will Reports be Good Enough to Turn Markets Positive?