-

Wal-Mart foreshadows good news ahead for retail earnings, and the possibility that consumers are still active despite record inflation

-

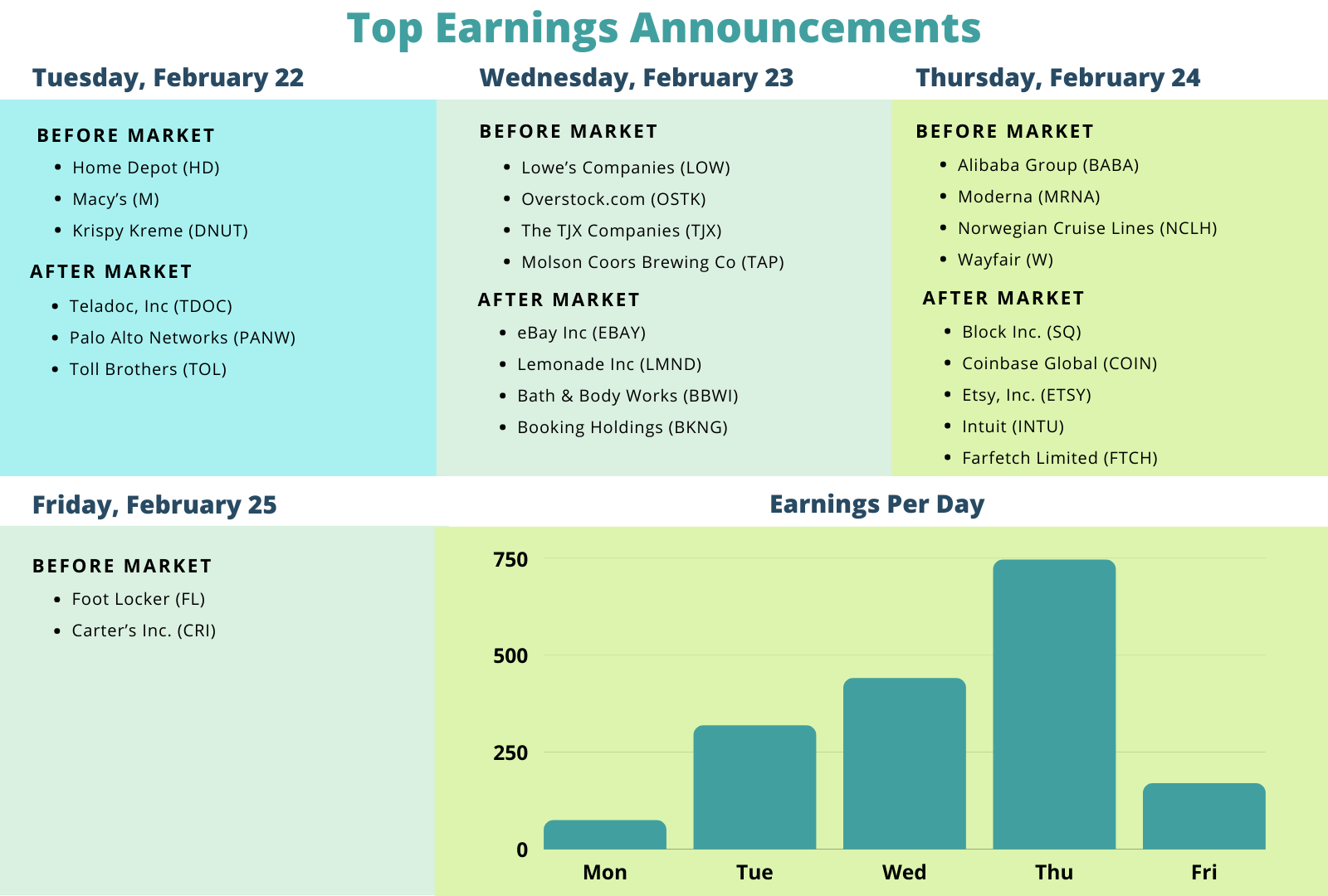

Retail earnings start in earnest this week with results from home improvement (HD, LOW), department stores (M) and travel & leisure (BKNG, NCLH)

-

Potential surprises this week: eBay and Molson Coors Brewing

-

Q4 peak earnings season set to conclude this week, with February 24 expected to be the busiest day

Wal-Mart Sets the Tone for Retailers this Week

As we head into the final peak week of the Q4 season, the retail earnings parade will be in full force. Retail earnings kicked off with Wal-Mart’s results on Thursday, beating top and bottom-line expectations and raising their dividend one penny (a trend we noted we are seeing more of this quarter). The world’s largest retailer is often seen as a bellwether for the reports that follow, and there were some interesting takeaways from Wal-Mart’s earnings call, particularly around inflation.

While consumers continue to digest the highest inflation in 40 years and the end of government stimulus, Wal-Mart remains confident in their ability to pass on higher costs to customers as they did in the latest quarter, noting that shopping trends have not changed. And despite continued supply-chain issues, WMT was able to increase global inventory 26% while other retailers continue to struggle to keep shelves stocked.

Some of Wal-Mart’s commentary was in contrast to what we’ve seen from other S&P 500 companies this season. According to FactSet, 75% of companies have mentioned the impact of inflation on recent results, mostly as a negative headwind. As more retailers report in the weeks to come, investors will be looking to see if those names are able to pass increased prices onto shoppers as well.

Overall EPS growth for the S&P 500 now stands at 30.9% (only up 0.6 percentage points since last week) with YoY revenues up 15.5%. (Data from FactSet

The Retail Parade Continues with Home Improvement Names and Department Stores

This week we will hear from other must-watch retailers such as Home Depot and Lowe’s. Both names continue to benefit from increased home improvement trends that started during the pandemic, and continue as home prices remain historically elevated. Typically when home prices rise we also see a jump in home improvement spending, as those being priced out of the market decide to stay in their current homes and go the renovation route.

Other names in this space include online home decor and furniture retailers. While they benefited from these trends in 2020 and 2021, many are now struggling. Wayfair and Overstock.com are both out this week, and after posting triple digit profit and/or sales growth during peak pandemic quarters are now expecting YoY decreases in revenues as they remain under pressure to show they can sustain the high growth figures they produced over the last two years. If Shopify’s results from last week are any indication, then expect other e-commerce retailers to be hard pressed to keep up with record results seen from the pandemic bump.

We also begin to hear from the department stores this week, starting with Macy’s tomorrow morning. Third quarter profit growth of 747% shocked even the most bullish analysts, as Macy’s was able to court younger customers by expanding into newer categories and improving their omni channel offering. Last week the stock rallied as Evercore ISI upgraded the retailer to outperform in part due to pent up apparel demand.

Companies in the travel and leisure space continue to report this week as well, as we look to results from Booking.com and Norwegian Cruise Lines. Get ready to see some quadruple digit growth rates on the back of improving travel demand – Booking is expected to report YoY EPS growth of 2440% after reporting in the red last year, and Norwegian is expecting top-line growth of 5869%. Hotels chains such as Hilton and Marriott blew expectations out of the water when they reported well above analyst estimates last week, and Airbnb (also surprising to the upside) noted that US and European booking lead times had returned to pre pandemic levels.

The overall Consumer Discretionary sector of the S&P 500 continues to lead on the bottom-line with YoY growth of 49.6%, but remains the fourth largest laggard on the top-line with only 11.4% growth. (Data from FactSet)

Chart data provided by Wall Street Horizon

Potential Surprises this Week - EBAY, TAP

eBay, Inc. (EBAY)

Company Confirmed Report Date: Wednesday, February 23, AMC

Projected Report Date (based on historical data): Wednesday, February 2

Z-Score: 7.91

Since 2006, eBay has reported Q4 earnings results in a range from January 18 - February 3, typically on a Tuesday or Wednesday. As such we set a report date of February 2. On January 24 the company confirmed they would report on February 23, three weeks later than we had anticipated based on their historical reporting range, suggesting there may be bad news shared on the upcoming call.

Before Q2 earnings we also noticed eBay had a high z-score when they confirmed a report date that was two weeks later than expected. However, we were aware that another possible reason for this could be due to recent management changes. In May, eBay issued a press release stating it would bring on a new CFO. Scott Priest, formerly CFO of Jetblue, officially took his new post on June 21. For Q3 the report date reverted to the historical norm.

Molson Coors Brewing Co (TAP)

Company Confirmed Report Date: Wednesday, February 23, BMO

Projected Report Date (based on historical data): Thursday, February 10

Z-Score: 7.81

Molson Coors Brewing has historically reported Q4 results anywhere from February 9 - 16, with no day of the week trend. As such we set a report date of February 10. On January 19 the company confirmed they would report on February 23, two weeks later than we had anticipated, suggesting results for the quarter may surprise to the downside.

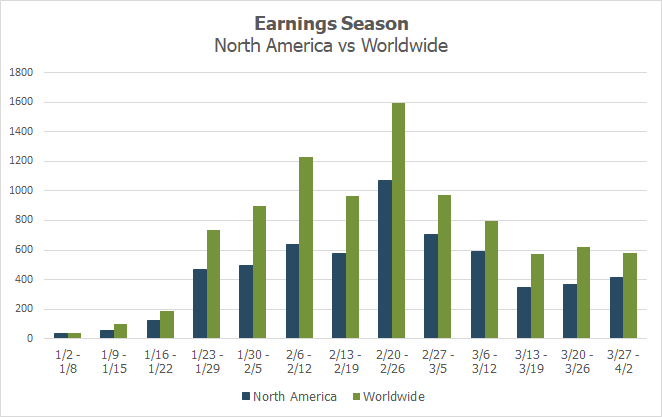

Earnings Wave

This week marks the final peak week of Q4 earnings season. February 24 is predicted to be the most active day with 746 companies anticipated to report. At this point 72% of companies have confirmed (out of our universe of 9,500+ global names).

Related Content

-

_thumb.png)

Volatility Watch: Eyeing a Pair of Blue Chips with Unusual Earnings Dates in the Heart of the Reporting Season

-

_thumb.png)

The Magnificent 7 Get Set to Report Amidst an S&P 500 Losing Streak

-

_thumb.png)

CEO Uncertainty Spikes After Improving Last Quarter

-

_thumb.png)

Earnings Season Heats Up, Spotting Two Unusual Reporting Dates in the Consumer Space

-

CNBC: Brace Yourself for Short-Term Volatility

-

Cheddar: It's Not Just You: The ‘Vibes Are a Little Off’ in This Economy

-

Data Minds - Triple Threat: Leveraging Data to Manage AI, ESG, and ETF Risks | April 11, 2024 [Recording Available]

-

_thumb.png)

Q1 2024 Earnings Preview: Will Reports be Good Enough to Turn Markets Positive?

-

[Podcast] Interactive Brokers: The Ins and Outs of Earnings Announcements

-

Pensions & Investments: U.S. companies increase buyback announcements