-

Equities have pulled back from their late July highs, though the Q2 reporting season has been solid

-

We spot three firms with unusual corporate event activity

-

A problem child is back at the top of our volatility watch list while an airline stock appears to see brighter skies ahead. Finally, one retail firm reports results this week, and it has a lot to live up to.

The summer stock market swoon has finally struck. Losses from the highs reached on the morning of July 27 have not been all that dramatic, however. Still, large caps and small caps, domestic and foreign equities, have pulled back as the dog days of August roll on. You can’t blame this mini-correction on earnings season – the S&P 500 EPS beat rate has been just shy of 80%, above the 5-year average.

For now, key clues come from individual company earnings events and corporate body language. We highlight a pair of unusual quarterly reports on tap along with a dividend resumption from a familiar low-cost airline.

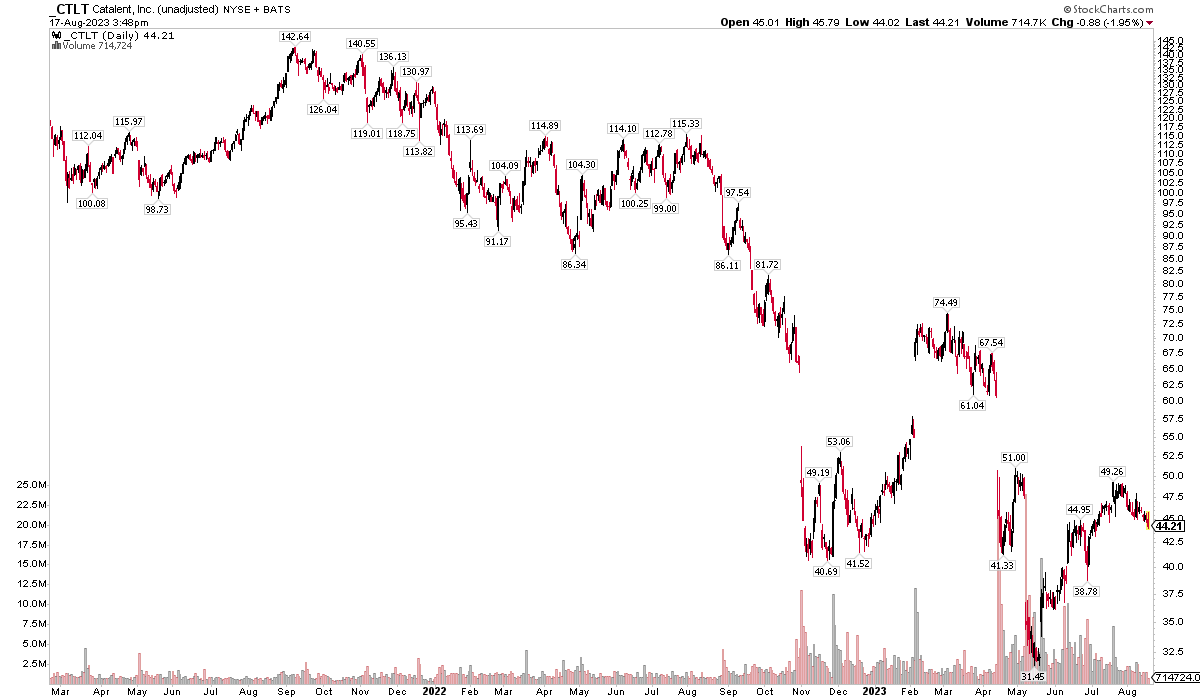

Catalent Resurfaces

First up is a troubled stock that has been on our radar before. Catalent (CTLT) is a global consumer health company that develops and manufactures solutions for drugs, protein-based biologics, cell, and gene therapies. The $8 billion market cap New Jersey-based Pharma industry stock within the Health Care sector has a history of late earnings date confirmations and pushing back its quarterly results.

This time around, our team again found that CTLT is late to confirm its Q4 report. The company normally confirms on July 27, plus or minus a standard deviation of 9.2 days. It has yet to confirm as of August 18. We have an unconfirmed earnings date of Tuesday, August 29 BMO, but there’s the risk that it could be pushed back if last quarter was any indication.

We first had a confirmed Q3 reporting date of May 9, but that was delayed time and again – CTLT did not post results until June 12. Ironically, the stock traded higher that day, but only after a massive plunge that took shares from $142 in late 2021 to just above $30 this past May.

Lower demand for its consumer discretionary products caused a guidance cut last November, sending shares crashing. CTLT then soared earlier this year amid takeover speculation, but those gains were fleeting as a reorg in April cast doubt on the firm’s long-term viability. Next, a guidance cut in May sparked a plunge to its year-to-date low. Finally, after another dismal outlook, Q2 results beat Street expectations back in June. A new CFO was named thereafter.

Then just recently, it was reported that activist Elliott Management had taken a stake in the embattled consumer health care stock – maybe a shakeup is just what CTLT needs.

CTLT: A Trouble Last Two Years, More Uncertainty Ahead of its Q4 2023 Results

Source: Stockcharts.com

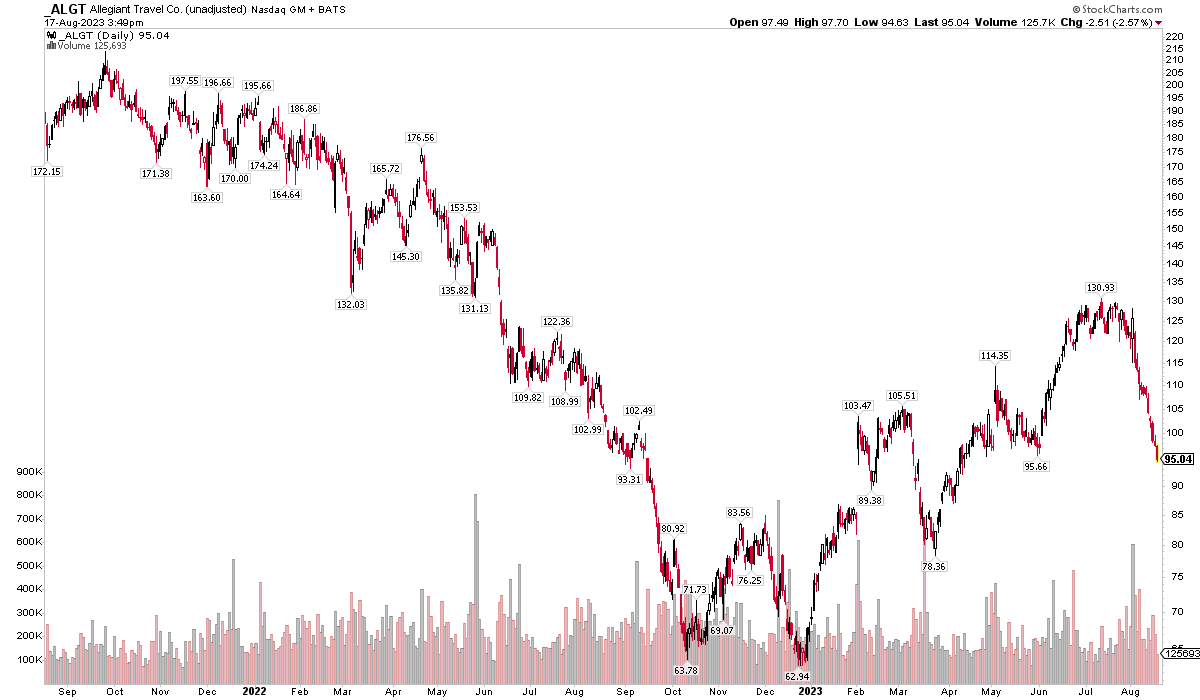

Allegiant Travel: An Optimistic Corporate Cue

That’s a lot of drama in CTLT. How about we lighten our load with a late-summer getaway? It could be time to climb aboard shares of Allegiant Travel (ALGT). The August 10th CPI report for July revealed concerning trends for the airline industry, though. Airfares prices are down about 8% from year-ago levels – perhaps that’s a sign that revenge travel demand is waning at long last. At the same time, BofA card data shows that total bookings remain stout, rising 10% year-over-year for the week ending July 30.

Stocks are discounting mechanisms, however, and ALGT has taken a nosedive from $131 a month ago to near $100 today. That descent comes as its management team announced a dividend resumption. On August 2 when the Industrials sector company released Q2 results, a $0.60 quarterly dividend ($2.40 annually) was reinstated. (The firm had suspended payouts around the onset of COVID-19 in early 2020.) That is a sanguine signal, but the stock has done anything but take off.

ALGT: A 2023 Winner, But August Turbulence Rattled the Bulls

Source: Stockcharts.com

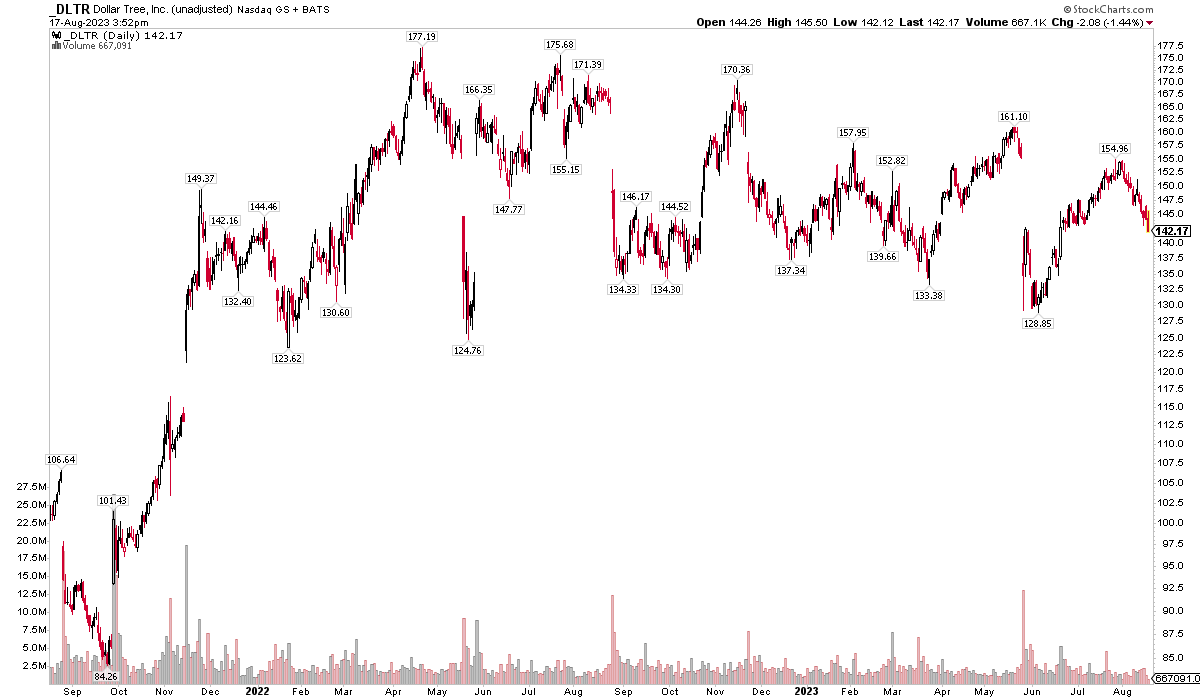

A Back-to-School Bargain Binge?

Finally, there’s no doubt more families are buying on the cheap at discount stores. The trade-down effect has been in full force since the onset of high inflation nearly two years ago. As a result, dollar stores have done well in terms of growing their earnings per share. Dollar Tree (DLTR) produced less than $6 of operating EPS in 2022, but in a preliminary earnings announcement this past June, the company now sees $10 of per-share profits doable by 2026. Thrifty consumers know that it’s more like “$1.25-tree” these days, but retail activity is still strong in its bare-bones stores.

There may be tailwinds now that inflation continues to cool off, though robust wage growth trends and a recent rise in oil and gas prices could cause profitability headwinds. We'll find out more when DLTR reports full Q2 2023 numbers on Thursday, August 24 BMO. The stock has been volatile, but sideways, since late 2021 as multiple contraction may attract value investors before long. 2024 could be a challenging year, though, with EPS expected to drop and as free cash flow hovers around the breakeven line.

DLTR: High Volatility Around Recent Earnings Events

Source: Stockcharts.com

The Bottom Line

As the stock market rally ebbs and with a tough stretch on the calendar, historically speaking, on the way, risk management is paramount. Be sure to recognize key events on the calendar that could spark volatility in your portfolio over the coming weeks.

Related Content

-

_thumb.png)

Spin-Off Stocks Surprise to Start Q2 - Reviewing Recent Market-Newcomers

-

MoneyFM: US Markets Wrap: Increase in Wall Street analysts’ Q2 S&P 500 earnings estimates

-

_thumb.png)

The Final Peak Week of the Q1 Season Begins Just As Earnings Hit Their Stride

-

_thumb.png)

Solar Stocks, Berkshire, and the latest Costco Craze

-

_thumb.png)

Big Tech Earnings Beats Stymie Q2 Sell-Off

-

_thumb.png)

Volatility Watch: Eyeing a Pair of Blue Chips with Unusual Earnings Dates in the Heart of the Reporting Season

-

_thumb.png)

The Magnificent 7 Get Set to Report Amidst an S&P 500 Losing Streak

-

_thumb.png)

CEO Uncertainty Spikes After Improving Last Quarter

-

_thumb.png)

Earnings Season Heats Up, Spotting Two Unusual Reporting Dates in the Consumer Space

-

CNBC: Brace Yourself for Short-Term Volatility