Key Takeaways:

-

S&P 500 blended EPS growth for Q4 increases for the first time in 3 weeks, now expected to come in at -4.9%.

-

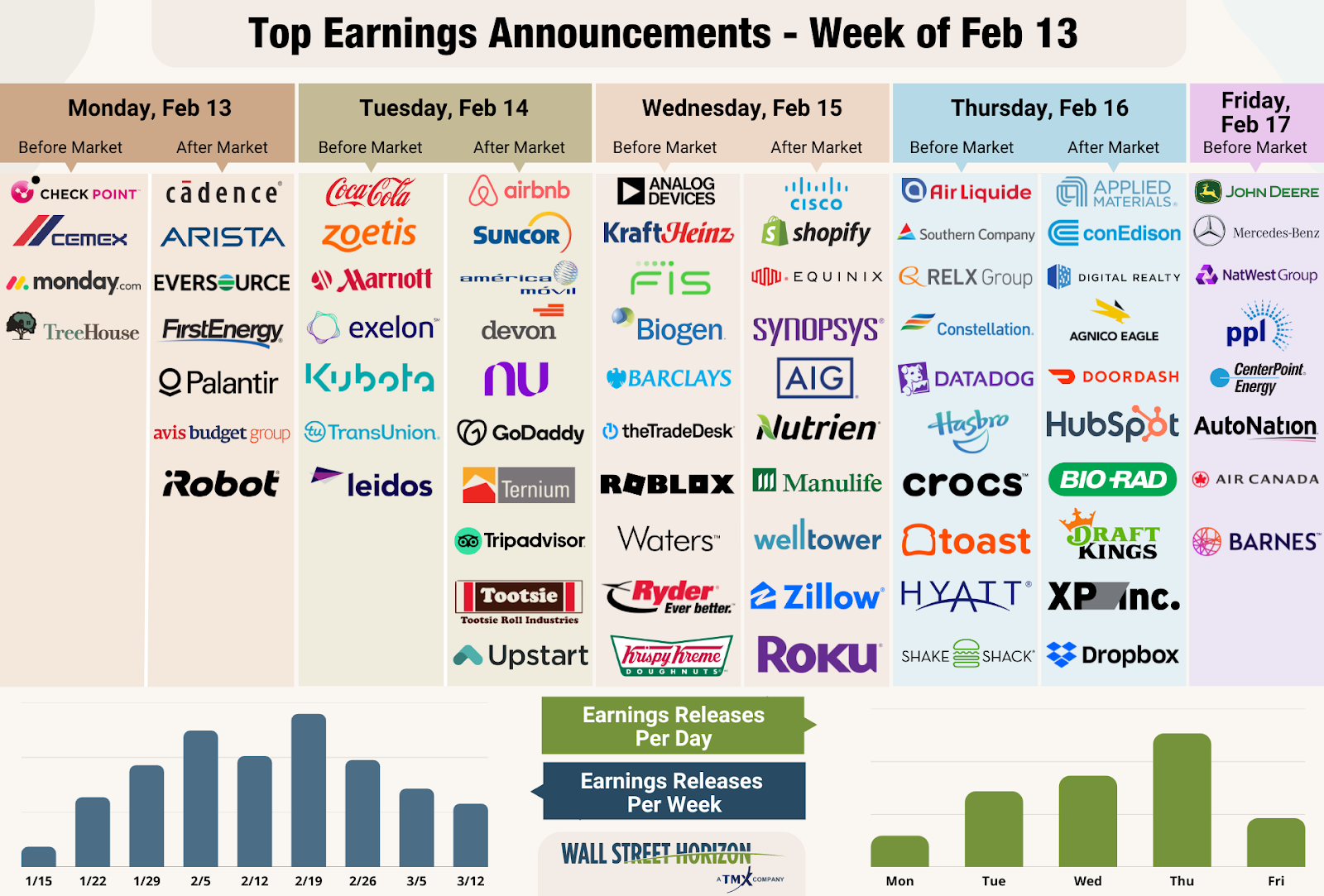

Peak earnings season rolls on this week with 1,276 global companies expected to report, as investors start to focus on Consumer Discretionary names

-

Potential surprises this week: BIIB

Last week US companies continued to report for the fourth quarter. The earnings season hasn’t been terrible thus far, but by no stretch of the imagination has it been wonderful either. Some standouts last week were within the consumer discretionary sector which gave some clues on the state of the US consumer, and provided a good backdrop for upcoming retail earnings.

A few restaurant names released results last week and revealed that inflation has US consumers trading down when they go out to eat, just as we have seen them trade down with retailers. Yum Brands! (YUM) managed to beat top and bottom-line expectations by large margins. The operator of Taco Bell, PizzaHut and KFC, saw quarterly same-store sales for those names increase 11%, 4% and 1%, respectively. Meanwhile, fast-casual chain Chipotle (CMG) announced last week that while their same-store sales increased 5.6%, they massively missed profit and revenue expectations. Restaurant names reporting in the coming week include: Denny’s Corporation (DENN), Shake Shack (SHAK), Bloomin’ Brands (BLMN), Texas Roadhouse (TXRH) and BJ’s Restaurants (BJRI).

We also got a preview into how retail might report when they start to release results in the next couple of weeks. Companies within the textiles, apparel, luxury goods subsector all reported better than expected results this week: Under Armour (UAA), VF Corporation (VFC), Ralph Lauren (RL), Tapestry (TPR). While that bodes well for the retailers they sell into, we still expect discount and off-price retailers to be the winners this quarter. Under Armour warned on their Q4 call that the current “promotional environment” will likely go deeper and last longer than many retailers would like, all in order to entice consumers. More apparel names report this week: Fossil (FOSL) and Crocs (CROX), but retailers don’t officially kick off until the week of February 20.

Due to some of those wins last week, overall S&P 500 EPS growth increased slightly to -4.9% from -5.3% in the week prior.

Peak Earnings Season Continues – Week 3 of 5

This marks the third peak week of the Q4 earnings season, with 1,276 companies (from our global universe of 9,500 equities) anticipated to release results, 61 of those coming from the S&P 500. We get a smattering of reports across different sectors this week, some names that will be garnering plenty of investor attention include: Coca-Cola (KO), Airbnb (ABNB), Cisco (CSCO), Shopify (SHOP), John Deere (DE), among others.

Source: Wall Street Horizon

Potential Surprises in the Week Ahead

This week we get results from a number of large companies on major indexes that have pushed their Q4 earnings dates outside of their historical norms. Seven companies within the S&P 500 confirmed outlier earnings dates for this week, five of which are later than usual and therefore have negative DateBreaks Factors*. Those five names are Howmet Aerospace (HWM), PerkinElmer (PKI), Waters Corp (WAT), Rollins Inc (ROL), and Biogen (BIIB). According to academic research, the later than usual earnings dates suggest these companies will report “bad news” on their upcoming calls. Eversource Energy (ES) and CenterPoint Energy (CNP) confirmed earlier than usual dates, suggesting they will report “good news” on their upcoming calls.

Biogen (BIIB)

Company Confirmed Report Date: Wednesday, February 15, BMO

Projected Report Date (based on historical data): Thursday, February 2

DateBreaks Factor: -3*

On January 18, Biogen confirmed a Q4 earnings date of February 15, nearly two weeks later than we had anticipated based on historical reporting trends. For the last 10 years BIIB has reported fourth quarter results from January 25 - February 3. Academic research suggests that the later than expected earnings date is a suggestion that bad news will be shared on the earnings call.

Biogen, whose leading portfolio of drugs treat Multiple Sclerosis, have seen sales in that segment drop in the last few quarters as multiple generic alternatives have launched in the US, Canada and some European markets. While current Wall Street estimates still have YoY EPS growing by 3% after many quarters of negative growth, revenues are expected to be down 11%.

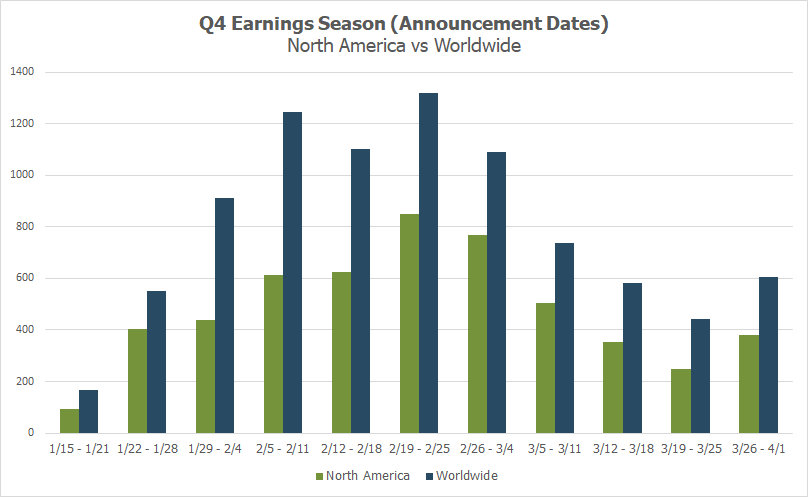

Earnings Wave - 69% Confirmed, 33% Reported (In our universe of 9,500 global equities)

This week marks the third week of Q4 peak earnings. This season peak weeks fall between January 30 - March 3, with each week expected to see over 1,000 reports. Currently February 23 is predicted to be the most active day with 685 companies anticipated to report.

Source: Wall Street Horizon

Related Content

-

_thumb.png)

Volatility Watch: Eyeing a Pair of Blue Chips with Unusual Earnings Dates in the Heart of the Reporting Season

-

_thumb.png)

The Magnificent 7 Get Set to Report Amidst an S&P 500 Losing Streak

-

_thumb.png)

CEO Uncertainty Spikes After Improving Last Quarter

-

_thumb.png)

Earnings Season Heats Up, Spotting Two Unusual Reporting Dates in the Consumer Space

-

CNBC: Brace Yourself for Short-Term Volatility

-

Cheddar: It's Not Just You: The ‘Vibes Are a Little Off’ in This Economy

-

Data Minds - Triple Threat: Leveraging Data to Manage AI, ESG, and ETF Risks | April 11, 2024 [Recording Available]

-

_thumb.png)

Q1 2024 Earnings Preview: Will Reports be Good Enough to Turn Markets Positive?

-

[Podcast] Interactive Brokers: The Ins and Outs of Earnings Announcements

-

Pensions & Investments: U.S. companies increase buyback announcements