-

S&P 500 EPS growth for Q2 2023 is set to come in at -7.1%, the lowest rate in 3 years and the third consecutive quarter of negative earnings growth

-

The LERI shows corporate uncertainty increasing to its highest level since the pandemic

-

Why are big tech names confirming their earnings dates so late? META, GOOGL

-

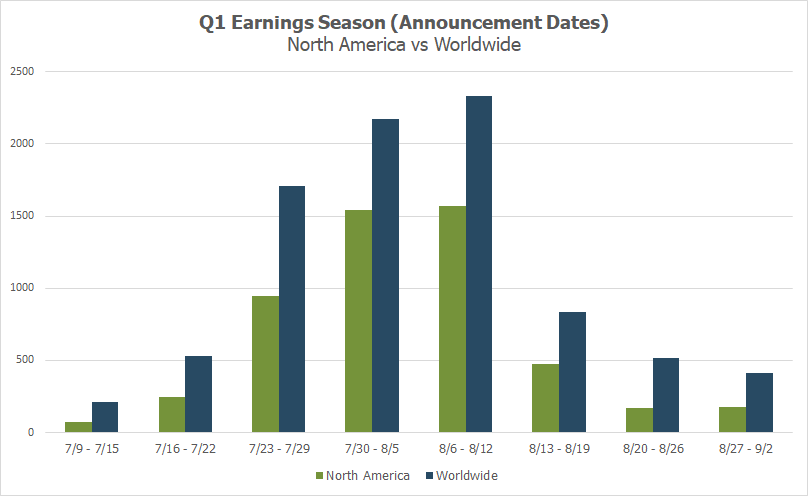

Peak weeks for Q2 season run from July 24 - August 11

Big Banks Seem Resilient, but Worries Still Pervade

Second quarter earnings season is off and running, and a few big banks set the tone when they reported on Friday. JPMorgan Chase (JPM) beat analyst expectations on both the top and bottom-line, while Citigroup (C) and Wells Fargo (WFC) only surpassed revenue expectations, while slightly missing EPS estimates.¹

Overall the results from banks, specifically JPM, are being seen as a sign that the economy is possibly more resilient than initially thought. Better-than-anticipated results stemmed from higher interest rates, prompting WFC to raise annual guidance for Net Interest Income (NII). JPM saw increases in lending and credit card transactions. Investment banking remained stable for JPM, however Citigroup reported that IB had yet to rebound.

Despite the better-than-expected results, there were still warnings from the CEOs of the world’s largest banks. All pointed robust Q2 results, but also risks ahead. Charlie Sharf, CEO of Wells Fargo suggested that the economy will continue to slow and that uncertainty remains. Jane Fraser of Citigroup mentioned a consumer that had been sitting on the sidelines since April. And Jamie Dimon, CEO of JPM and one of the most closely listened to banking execs, highlighted ongoing issues from inflation to unprecedented rate tightening, as well as a consumer that was still spending but “slowly using up their cash buffers.” Comments like those seemed to mute the initial bullish reaction from investors, with Citigroup’s stock down 4.7% since the report, Wells Fargo’s is flat and only JPM getting a boost.

The overall S&P 500 blended EPS growth rate improved slightly to -7.1% from -7.2% the week prior.² This could be the lowest growth rate since Q2 2020. Leading sectors this quarter include Consumer Discretionary and Communication Services while Materials and Energy are expected to be laggards.

LERI Update – CEOs the Most Uncertain They’ve Been Since the COVID-19 Pandemic

The official pre-peak reading of the Late Earnings Report Index (LERI) showed that CEOs continue to be hesitant ahead of the second quarter earnings season.

The Late Earnings Report Index tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, anything above that indicates companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests companies feel they have a pretty good crystal ball for the near-term.

The current pre-peak season LERI reading stands at 132, the highest reading since the COVID-19 pandemic. As of July 14, there were 38 late outliers and 26 early outliers. Typically, the number of late outliers trends upwards as earnings season continues, indicating that the LERI is poised to get even worse from here as corporations are increasingly more worried heading into the second half of the year.

Source: Wall Street Horizon

On Deck This Week

This week we’ll see more results from banks, including investment banks Goldman Sachs and Morgan Stanley. This should shed more light on the current state of deal activity, as these names have already hinted to disappointing results. We’ll also hear from regional banks such as Western Alliance, US Bancorp, Citizens, Comerica, and more. Investors will want to see if they have recovered from the regional banking contagion that hit in late Q1.

Highly-watched names such as Netflix, Tesla and IBM will also be out with Q2 reports this week.

Source: Wall Street Horizon

Why Are Big Tech Names Confirming Their Earnings Dates Later Than Usual?

A couple of big tech names made their way onto our radar with late confirmation timing.

Released in 2022, Confirmation Timing uses historical data to project an expected confirmation date and the normal range that enables the identification of:

-

Companies that have not yet confirmed an earnings date and are materially late compared to their historical trends/behaviors.

-

Announced earnings dates in which the Confirmation Timing is materially earlier or later than the company’s historical average of the same quarter.

Wall Street Horizon findings show there is valuable information to be gained by analyzing Confirmation Timing events and has seen that firms reporting earlier than usual exhibit positive abnormal returns. Likewise, companies that confirm later than average typically exhibit negative abnormal returns.

Meta Platforms (META)

In recent years META has confirmed its Q2 earnings date around July 2 with a standard deviation of +/- 0.8 days. For Q2 2023, Meta ended up confirming their earnings date on July 6, four days past their mean confirmation day. While the earnings date itself, July 26, is within the historical range of expected earnings dates, the delay in confirming that date could point to a hesitant management team and possibly indicate bad news will be shared on the call. This is valuable corporate body language for current or interested META investors.

Alphabet Inc. (GOOGL)

In recent years GOOGL has confirmed its Q2 earnings date around June 28, with a standard deviation of +/- 12.3 days. Today (July 17) GOOGL is 19 days past mean confirmation day. While google has a larger standard deviation of 12.3 days, they are now a week outside of that range.

Again, why is this significant? Companies that tend to stall on confirming their earnings dates also tend to set later than usual earnings dates which academic research has shown highly correlates to bad news being shared on the call. While estimates for GOOGL currently look strong, actual results and/or outlook could differ.

Q2 2023 Earnings Wave

This season peak weeks will fall between July 24 - August 11, with each week expected to see nearly 2,000 reports or more. Currently August 3 is predicted to be the most active day with 1,028 companies anticipated to report. Thus far only 52% of companies have confirmed their earnings date (out of our universe of 9,500+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

Source: Wall Street Horizon

¹ Using analyst estimates from FactSet

² https://advantage.factset.com/hubfs

Related Content

-

_thumb.png)

Solar Stocks, Berkshire, and the latest Costco Craze

-

_thumb.png)

Big Tech Earnings Beats Stymie Q2 Sell-Off

-

_thumb.png)

Volatility Watch: Eyeing a Pair of Blue Chips with Unusual Earnings Dates in the Heart of the Reporting Season

-

_thumb.png)

The Magnificent 7 Get Set to Report Amidst an S&P 500 Losing Streak

-

_thumb.png)

CEO Uncertainty Spikes After Improving Last Quarter

-

_thumb.png)

Earnings Season Heats Up, Spotting Two Unusual Reporting Dates in the Consumer Space

-

CNBC: Brace Yourself for Short-Term Volatility

-

Cheddar: It's Not Just You: The ‘Vibes Are a Little Off’ in This Economy

-

Data Minds - Triple Threat: Leveraging Data to Manage AI, ESG, and ETF Risks | April 11, 2024 [Recording Available]

-

_thumb.png)

Q1 2024 Earnings Preview: Will Reports be Good Enough to Turn Markets Positive?