Key Takeaways:

-

S&P 500 EPS growth for Q1 2023 is set to come in at -6.8%, the lowest rate in nearly 3 years

-

Themes from Q1 and for CY 2023: inflation, increasing interest rates, possibility of recession, banking crisis, softening employment

-

The LERI shows corporate uncertainty increasing to a 2-year high

-

First Republic and PacWest suggest bad news ahead on Q1 calls

-

Peak weeks for Q1 season from April 24 - May 12

This Friday, April 14, marks the unofficial kick-off of Q1 2023 earnings season, and early estimates are pointing to a second consecutive quarterly drop in year-over-year S&P 500 EPS growth, otherwise known as an earnings recession. Currently S&P 500 earnings are expected to fall 6.8%¹ YoY, the largest decline since the depths of COVID lockdowns in Q2 2020.

After initially starting out with an expected decrease of 4.1%, the fourth quarter 2022 earnings season ended with an even steeper YoY EPS decline of -4.6%. Historically, the S&P 500 YoY earnings growth figure increases as the season gets underway and more companies report (and beat!) analyst expectations. Analysts tend to be more bullish on longer-term earnings expectations, three to four quarters out. However, as the current quarter approaches and companies release updated (and typically very conservative) guidance, they begin to draw estimates down. The sell side does this by such a large margin that the majority of companies are able to beat estimates, the 10-year average beat rate according to FactSet is 73%, and therefore the growth rate expands.

What are analysts seeing that caused them to lower Q1 expectations from -0.3%¹ on December 31, to -6.8% today? Many of the same headwinds mentioned on earnings calls in the back half of 2022 will again be the focus of Q1 reports: stubbornly high inflation, higher interest rates, possibility of recession .. likely with the addition of a couple of new concerns: the possibility of more bank failures and the softening labor market.

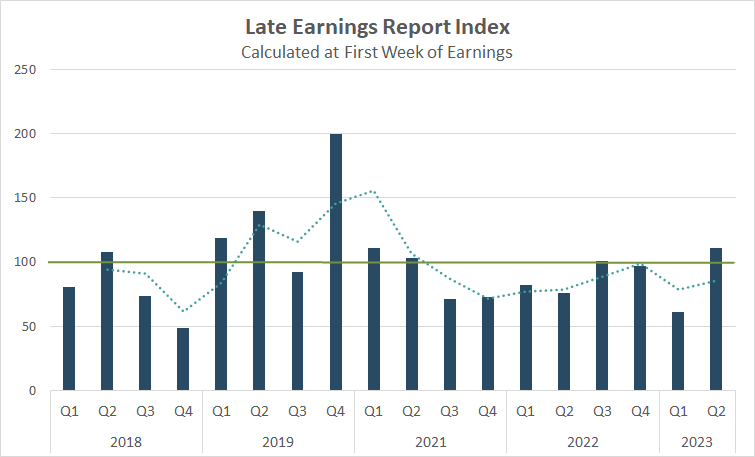

LERI Shows CEO Uncertainty Is at Its Highest Level Since Q1 2021

Not only do analysts look more uncertain about Q1 earnings season, but early signs show companies aren’t feeling that great either.

The Late Earnings Report Index (LERI) tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, anything above that indicates companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests companies feel they have a pretty good crystal ball for the near-term.

While we won’t officially calculate the Q1 2023 earnings season (reporting in Q2 2023) LERI until the big banks (JPM, WFC, C) report Friday, April 14, the current pre-peak LERI reading stands at 111, the highest reading in two years. As of April 12, there were 31 late outliers and 25 early outliers. Typically, the number of late outliers trends upwards as earnings season continues, indicating that the LERI is poised to get even worse from here as corporations are increasingly more worried heading into the second half of the year.

Source: Wall Street Horizon. Our data is locked based on which companies in our universe had market caps of $250M or higher at the beginning of each quarter.

Potential Earnings Surprises - First Republic Bank and PacWest Signal Bad News Ahead

These two regional banks would typically report earnings in the same week as the big banks, but delayed earnings dates for FRC and PACW could signal more trouble ahead for the embattled regional banks. Warren Buffet said it today in an interview with CNBC, “we’re not through with bank failures”... and this data could indeed confirm that the banking crisis is not over.

Academic research shows when a corporation reports earnings later in the quarter than they have historically, it typically signals bad news to come on the conference call. The reverse is also true, an early earnings date suggests good news will be shared. The idea is that you’d prefer to delay bad news, but when you have good news you want to run out and share it.

First Republic Bank (FRC)

Company Confirmed Report Date: Monday, April 24, AMC

Projected Report Date (based on historical data): Thursday, April 13, BMO

DateBreaks Factor: -3*

On Friday, April 7, First Republic Bank (FRC) announced they would report Q1 2023 earnings on April 24 after market close. This is 11 days later than expected, the first Monday report ever and the first after-the-bell report ever. This also pushes quarterly earnings results past FRC’s monthly options expiration date of April 21, meaning options holders will have less information when deciding whether or not to exercise without having the important details shared on the earnings call.

It probably comes as no surprise that First Republic Bank might want to delay their earnings results after a whirlwind first quarter. The 14th largest regional bank in the United States has become one of the focal points of the banking crisis. After the collapse of Silicon Valley Bank provoked panicked withdrawals from various regional banks, JPMorgan Chase along with 10 other large banks bailed out First Republic with $30B in backstop funds.

That massive measure hasn’t seemed to help, however, as the following day FRC announced they were suspending their dividend on common stock, and earlier this week they announced they were also suspending their dividend on preferred stocks. The stock is down 88% YTD.

PacWest Bancorp (PACW)

Company Confirmed Report Date: Tuesday, April 25, AMC

Projected Report Date (based on historical data): Thursday, April 20

DateBreaks Factor: -3*

Another west coast, mid-sized bank, PacWest Bancorp has delayed their earnings date for Q1 in the midst of the regional banking crisis. On March 31, PACW confirmed they would report Q1 financial results on Tuesday, April 25, a week later than usual. Like FRC, this also pushed past the monthly options expiration date of April 21.

Just a week prior to confirming their Q1 earnings date, PACW provided a rather sobering update to investors which detailed how customers had withdrawn 20% of their deposits YTD, as well as information around its $1.4B capital raise from Atlas SP Partners. The bank has lost over half of its market value since the beginning of the year.

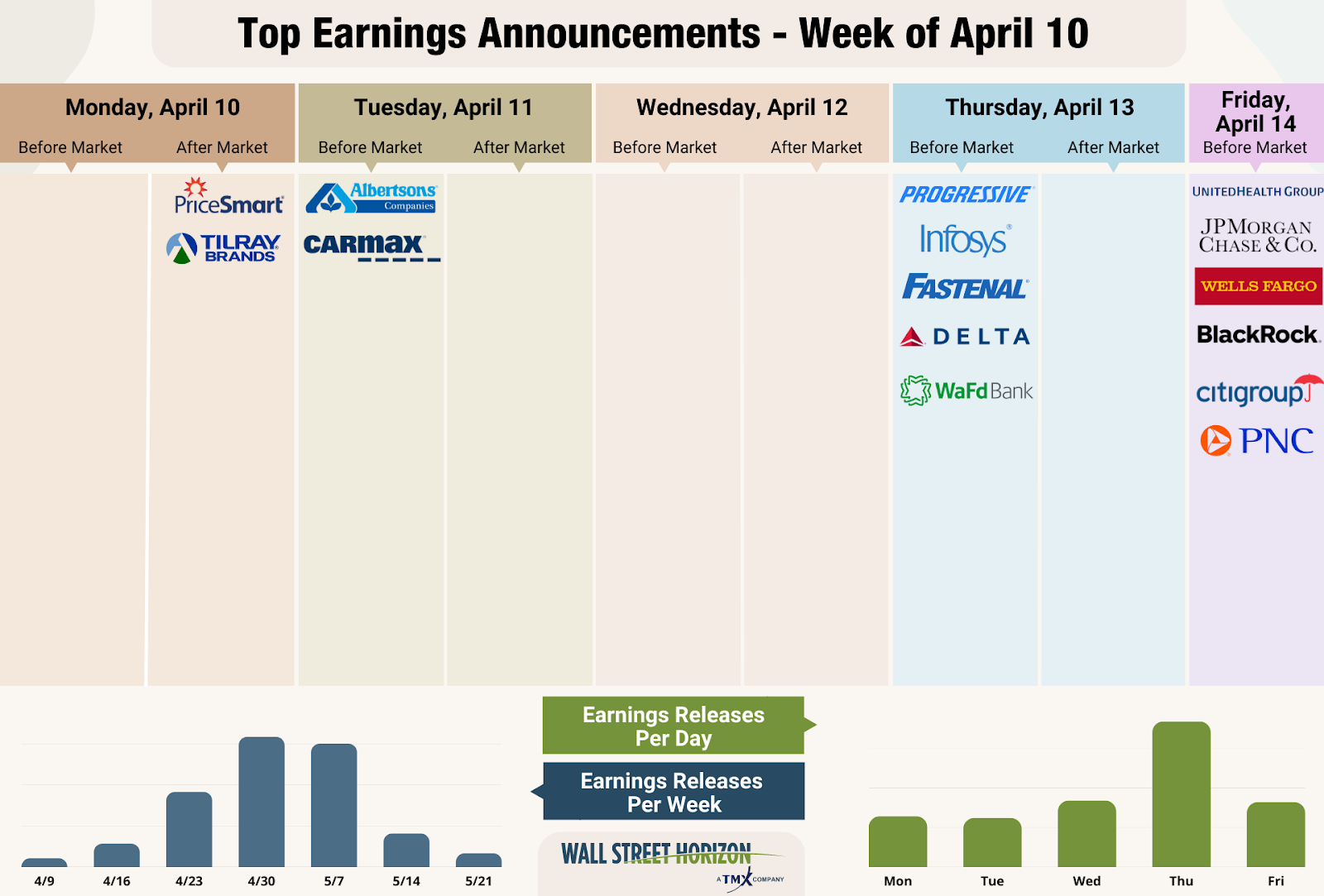

On Deck this Week: DAL, JPM, WFC, C

Source: Wall Street Horizon

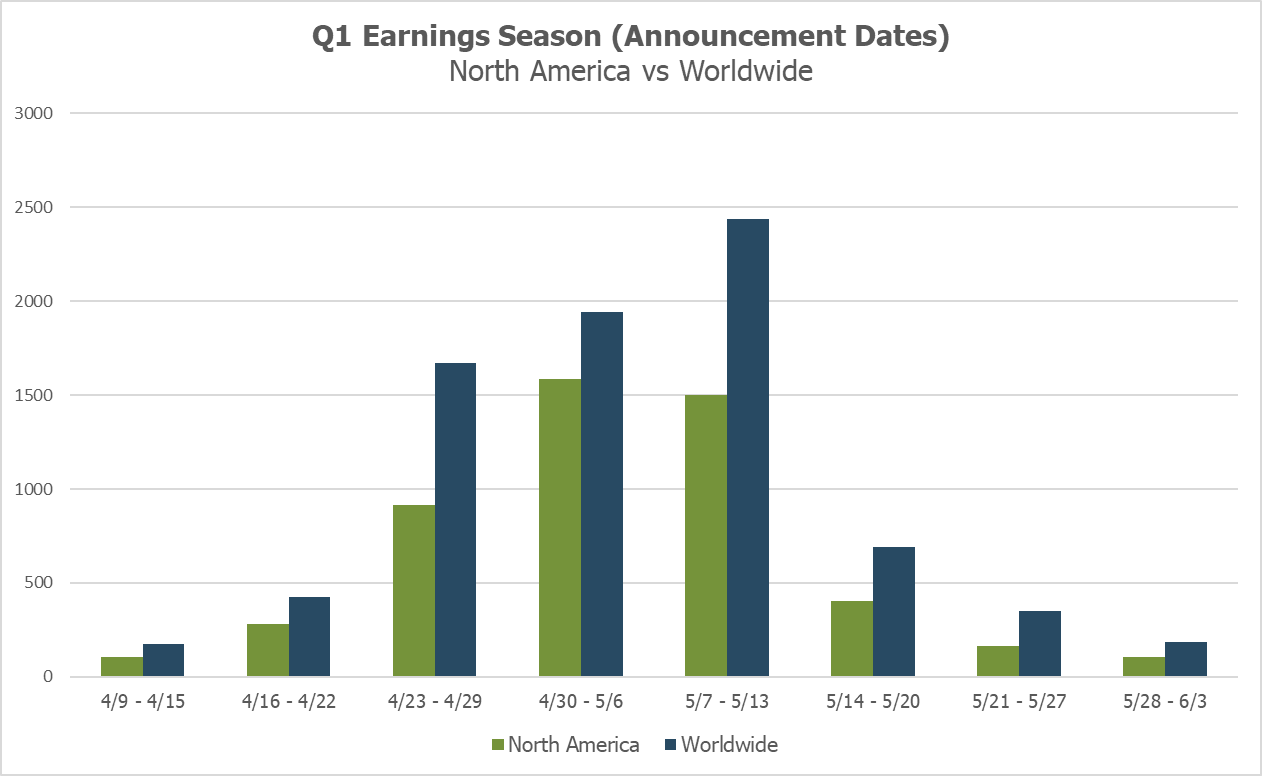

Q1 Earnings Wave

This season peak weeks will fall between April 24 - May 12, with each week expected to see over 1,000 reports. Currently May 11 is predicted to be the most active day with 986 companies anticipated to report. Thus far only 45% of companies have confirmed their earnings date (out of our universe of 9,500+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

Source: Wall Street Horizon

¹ https://advantage.factset.com/

* Wall Street Horizon DateBreaks Factor: statistical measurement of how an earnings date (confirmed or revised) compares to the reporting company's 5-year trend for the same quarter. Negative means the earnings date is confirmed to be later than historical average while Positive is earlier.

Related Content

-

_thumb.png)

CEO Uncertainty Spikes After Improving Last Quarter

-

_thumb.png)

Earnings Season Heats Up, Spotting Two Unusual Reporting Dates in the Consumer Space

-

Data Minds - Triple Threat: Leveraging Data to Manage AI, ESG, and ETF Risks | April 11, 2024 [Recording Available]

-

_thumb.png)

Q1 2024 Earnings Preview: Will Reports be Good Enough to Turn Markets Positive?

-

[Podcast] Interactive Brokers: The Ins and Outs of Earnings Announcements

-

Pensions & Investments: U.S. companies increase buyback announcements

-

_thumb.png)

Shareholder Meetings in Focus as Earnings Season Begins

-

_thumb.png)

Q2 2024 Investor Conference & Events Highlights

-

_thumb.png)

Q1 2024 Buyback and Dividend Increases Point to Improving Corporate Sentiment

-

MoneyFM: US Markets Wrap: What's driving the sunny outlook of CEOs and investors?