- Equity markets rally as earnings season progresses.

- An impressive EPS beat rate overshadows bearish concerns.

- Global economic growth set to surge in 2021 as the US Dollar falls Q1

- Health-related stocks with unusual earnings dates are in focus

Stock Surge in February

Equities followed an eventful January with massive gains during the first half of February. Small caps continue to lead while global stocks keep pace with the S&P 500. Sector-wise, Energy keeps on leading after the beaten-down group was the worst performer in 2020. What’s interesting over the last few weeks is the comeback in mega cap tech stocks. The group, including stalwarts in the Communication Services and Consumer Discretionary sectors (Google, Facebook, and Amazon), are outperforming the total US market following several months of lackluster relative performance. Sector rotation amid a broad uptrend has been the theme.

Small cap strength is another important feature – investors were caught off guard when the Russell 2000 index jumped in early November. The index of small issues has more than doubled off the March 2020 low. Why the outperformance? History shows that small caps tend to outperform large caps coming out of recessions. Could there be more gains? Momentum is on the side of the bulls and domestic small caps often do well when US GDP runs high.

GDP Expected to Rise

Global economic growth should improve as 2021 wears on. Bank of America Global Research predicts that the US economy will expand by 6.0% while global GDP is forecast to climb 5.5%. Vaccination rollouts and overall improving COVID-19 trends recently in the US and the Big 5 European countries suggests these bullish predictions could come to fruition. Much depends on how consumers react once normalcy slowly returns. There is the threat of another jump in COVID-19 cases later this quarter according to the latest Institute for Health Metrics and Evaluation (IHME) model due to new strains of the virus side-stepping the various vaccines currently available. Investors will want to monitor the latest developments and comments from Health Care companies as we continue to fight the virus.

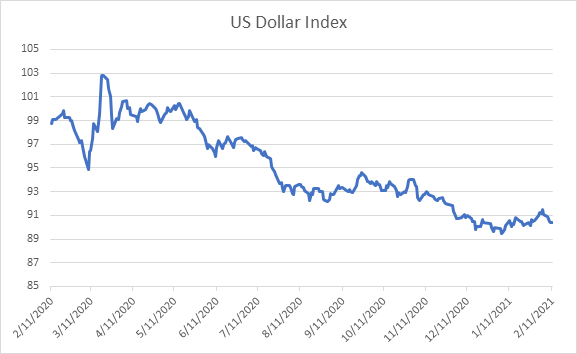

Dollar Drops, Boosting US Corporate Earnings

The US Dollar Index (DXY) is up fractionally on the year, but is down about 4% from early November. That is a sizable move in the currency markets. We have all been witness to the meteoric rise in cryptocurrencies during the last several weeks as Bitcoin surpasses $40,000 and the latest talk of the street, Dogecoin, surges. Highly speculative traders can get their kicks in the crypto space, but other portfolio managers eye how the USD, Euro, and Yen impact corporate operations and profits.

Figure 1: US Dollar Index 1-year chart

Earnings Season Update

The DXY’s drop means US companies are slightly more profitable as US goods become relatively cheaper overseas. Bank of America notes that the weaker DXY boosted US corporate earnings by about 1% in Q4 2020. The small leg-up helped S&P 500 operating earnings turn positive on a year-over-year basis. Few pundits expected a y/y gain in EPS even just a few months ago, but Corporate America was resilient during the pandemic. Stimulus and vaccine-hopes certainly helped.

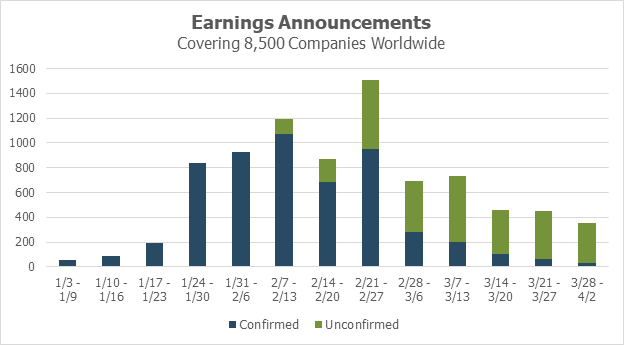

Q4 2020 is yet another fantastic earnings period relative to analyst expectations, buttressing strong Q2 and Q3 results versus estimates. Only the Energy sector failed to beat expected earnings. Several of the biggest sectors posted aggregate profits more than 20% above consensus, according to Bank of America. What’s more, stock price reactions have improved following dismal next-day and 5-day equity performances among the beaters earlier this earnings season. Profit-taking was the name of the game in January, but that theme has reversed slightly as equity markets have been on the rise this month.

We feature Health Care this week in our review of earnings outliers. The sector has performed well in terms of EPS versus the Wall Street consensus. 71% of companies in the S&P 500 Health Care sector beat on both sales & EPS already, according to BofA.

Earnings season continues to be busy through next week, but then tapers in March.

Figure 2: Wall Street Horizon earnings announcements

Earnings Outliers - OPK & HTA

This week we feature two stocks, one in the Health Care sector and the other a Health Care REIT.

OPKO Health Inc (OPK) is one options traders should keep on their radar. On October 30, Wall Street Horizon set an unconfirmed Q4 earnings date of February 24 (after market) based on the firm’s historical reporting trends. The company usually reports between February 26 and March 1 with no day of the week trend. OPK issued a press release on February 3 at 9:01 am stating results would be released on Thursday, February 18 (after market). Wall Street Horizon alerted clients to the change. The sooner than expected earnings date resulted in a high Z-score of -7.4 and crossed the February 19 options expiration date.

OPK could report unusual news to investors following the story last week that the firm’s Chief Accounting Officer resigned. OPK said in its 8-K/A filing* , “Mr. Hernandez’s resignation is not a result of any disagreement with the Company on any matter relating to the Company’s operations, policies or practices.” Shares of OPK continue to perform well, up 250% from a year ago.

Healthcare Trust of America (HTA) is another one to watch. On November 4, Wall Street Horizon set an inferred Q4 earnings date of February 11 based on the company’s historical reporting trends. HTA has a history of reporting Q4 results between February 13-15 with no day of the week trend. On February 3, the firm issued a press release stating quarterly results would be released on Monday, February 22 (after market). We notified clients of the change immediately. The later than usual earnings date results in a high Z-score of 3.58 and crossed the February 19 monthly options date.

REITs felt the brunt of the COVID-crash, but like many sectors, it all depends on the industry and niche. The relative winners include Industrial, storage, and specialty REITs while the relative losers are found in the residential and office spaces. Health Care REITs are a mixed bag, and HTA’s stock performance suggests it has been a slow recovery as the stock is down slightly over the last 52 weeks.

*https://info.wallstreethorizon.com/e/787713/4480921000009-opk-20210201-htm/4s5y2/164919053?h=aKd2imZFkyi_IP672sRWYmvImWVXJ0eJVpnZ2YBeoEA

Conclusion

Equity market dips have been quickly bought since November while volatility runs above the long-term average. A general upward trend in stock prices continues despite many calls for an over-valued market and an over-extended rally. A positive earnings season certainly bolstered the bulls’ case. Positive EPS trends and optimistic executives appear to over rule the bearish narratives for now. Traders must monitor key breaking news events from the corporate world as earnings season slows down. Wall Street Horizon alerts clients to market-moving data in this fast-paced environment.

Recent Content

-

See It Market: CEO Uncertainty Rising As Q1 Earnings Season Ends Better Than Expected

-

_thumb.png)

Mid-Q2 2024 Investor Conference & Events Highlights Update

-

Fox Business: Watch 'corporate body language' for earnings clues

-

Cheddar: Earnings Season Takeaways? Companies Are Doing… Pretty Well!

-

Yahoo Finance: Mid-Q2 2024 Investor Conference and Events Highlights Update

-

_thumb.png)

CEO Uncertainty Remains High Even As Q1 Earnings Season Ends Better-than-Expected

-

Tabb Forum: Spin-Off Stocks Surprise to Start Q2 – Reviewing Recent Market-Newcomers

-

_thumb.png)

Spin-Off Stocks Surprise to Start Q2 - Reviewing Recent Market-Newcomers

-

MoneyFM: US Markets Wrap: Increase in Wall Street analysts’ Q2 S&P 500 earnings estimates

-

_thumb.png)

The Final Peak Week of the Q1 Season Begins Just As Earnings Hit Their Stride